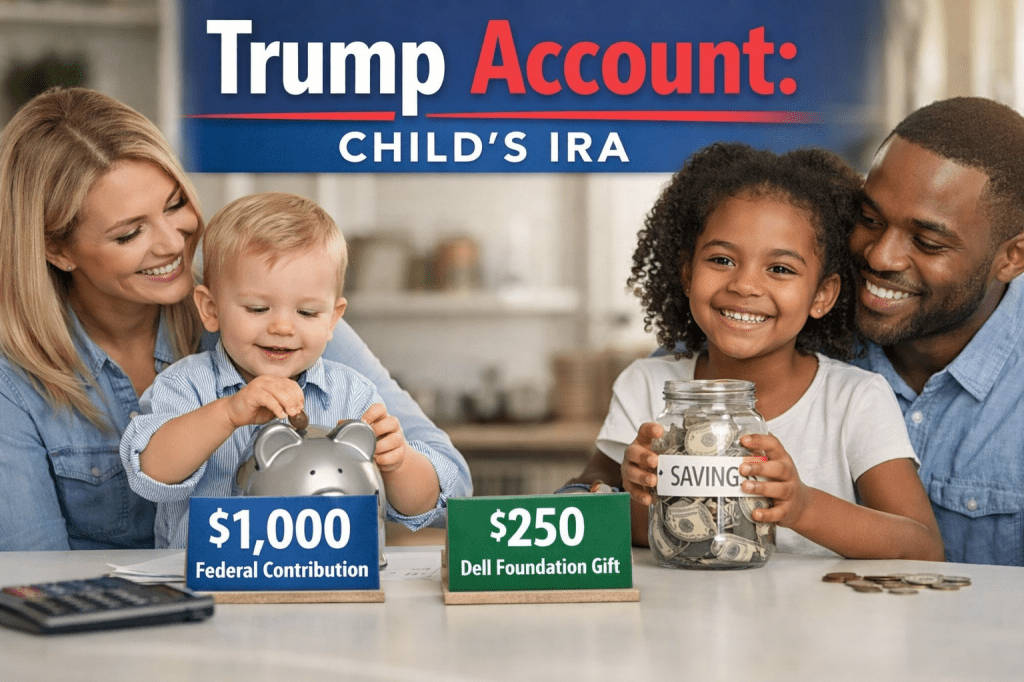

Trump Accounts are a new type of child savings vehicle created under federal law. If you have a child under 10, there’s also a separate philanthropic initiative (backed by Michael and Susan Dell) that may fund a $250 deposit into eligible children’s accounts—but the rules differ depending on whether your child qualifies for the federal $1,000 pilot contribution or the Dell-funded $250 deposit.

1. What is a Trump Account?

A “Trump Account” is the colloquial name for a proposed tax-advantaged savings vehicle—likely structured as a Universal Savings Account (USA) or an expanded 529 Education Savings Account. These accounts are designed to allow families to save for a child’s future with tax-free growth. Unlike traditional savings accounts, the earnings on these funds are typically not taxed as long as they remain in the account or are used for qualified expenses, providing a powerful tool for compound growth over the child’s lifetime. Important IRS features:

- During the “growth period” (generally until December 31 of the year before the child turns 18), special rules apply (investment limits, contribution rules, and distribution restrictions).

- No deduction is allowed for contributions to a Trump account (so you don’t “write off” deposits on your tax return).

- No contributions can be made before July 4, 2026 (this includes the federal pilot deposit).

2) Who is gifting the $250 to the Trump account for children under 10?

The proposed $250 “kickstart” gift is intended to be a federally funded seed deposit provided by the U.S. Department of the Treasury. The goal of this incentive is to encourage low-to-middle-income families to begin the habit of long-term investing.. The $250 is a philanthropic initiative funded by Michael and Susan Dell (often discussed in media as “Dell funding” tied to Trump Accounts / Invest America accounts).

3. How do Children Under 11 Qualify?

Based on current policy drafts, the primary qualifications for the $250 incentive are:

- The child must be apart of the first 25 million American children age 10 and under to create a Trump account.

- Age Requirement: The child must be 10 or younger at the time the account is established.

- Social Security Number: The child must have a valid Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Income Thresholds: The incentive will be provided by households that live in zip codes with median incomes below $150,000.

- U.S. Residency: The child must meet the standard U.S. residency requirements used for the Child Tax Credit (living with the taxpayer for more than half the year).

4. How to claim your Trump Account on your 2025 taxes.

Registering a child for a Trump Account during tax filing

Taxpayers will be able to opt into the Trump Account program while filing their 2025 taxes.

- Parents can elect to create a Trump Account for their child during the tax filing process by using form 4547.

- If you don’t want to file the form with your taxes, you can submit form 4547 at anytime via online portal that is scheduled to be available in the summer of 2026.

- The IRS has stated that contributions—including the federal $1,000 and private $250—cannot be deposited until after July 4, 2026.

Accuracy Matters: Please be advised that “Trump Accounts” and the associated $250 gift are subject to finalized federal legislation and IRS implementation. At this time, there is no line on the 2024 or 2025 Form 1040 labeled “Trump Account.” We recommend maintaining records of your child’s SSN and birth certificate now, so you are ready to move quickly once the program is officially active.

Questions about your family’s eligibility? Contact Howard Tax Prep LLC today—We fix tax problems (and help you plan for the future).