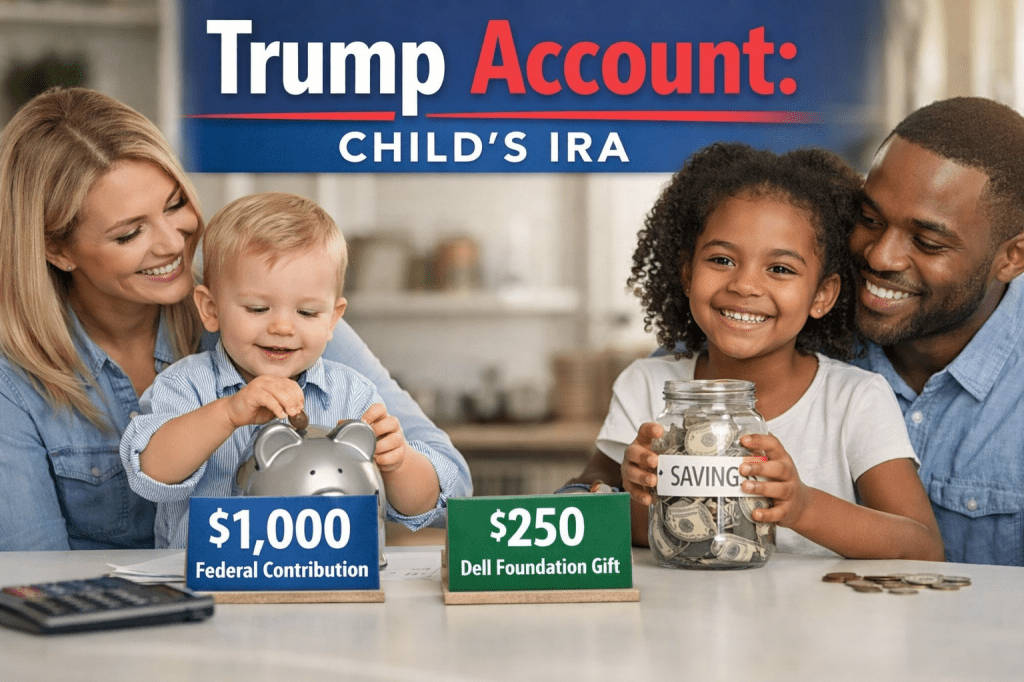

Trump Accounts are a new type of child savings vehicle created under federal law. If you have a child under 10, there’s also a separate philanthropic initiative (backed by Michael and Susan Dell) that may fund a $250 deposit into eligible children’s accounts—but the rules differ depending on whether your child qualifies for the federal $1,000 pilot contribution or the Dell-funded $250 deposit.

1. What is a Trump Account?

A “Trump Account” is the colloquial name for a proposed tax-advantaged savings vehicle—likely structured as a Universal Savings Account (USA) or an expanded 529 Education Savings Account. These accounts are designed to allow families to save for a child’s future with tax-free growth. Unlike traditional savings accounts, the earnings on these funds are typically not taxed as long as they remain in the account or are used for qualified expenses, providing a powerful tool for compound growth over the child’s lifetime. Important IRS features:

During the “growth period” (generally until December 31 of the year before the child turns 18), special rules apply (investment limits, contribution rules, and distribution restrictions).

No deduction is allowed for contributions to a Trump account (so you don’t “write off” deposits on your tax return).

No contributions can be made before July 4, 2026 (this includes the federal pilot deposit).

2) Who is gifting the $250 to the Trump account for children under 10?

The proposed $250 “kickstart” gift is intended to be a federally funded seed deposit provided by the U.S. Department of the Treasury. The goal of this incentive is to encourage low-to-middle-income families to begin the habit of long-term investing.. The $250 is a philanthropic initiative funded by Michael and Susan Dell (often discussed in media as “Dell funding” tied to Trump Accounts / Invest America accounts).

3. How do Children Under 11 Qualify?

Based on current policy drafts, the primary qualifications for the $250 incentive are:

The child must be apart of the first 25 million American children age 10 and under to create a Trump account.

Age Requirement: The child must be 10 or younger at the time the account is established.

Social Security Number: The child must have a valid Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

Income Thresholds: The incentive will be provided by households that live in zip codes with median incomes below $150,000.

U.S. Residency: The child must meet the standard U.S. residency requirements used for the Child Tax Credit (living with the taxpayer for more than half the year).

4. How to claim your Trump Account on your 2025 taxes.

Registering a child for a Trump Account during tax filing

Taxpayers will be able to opt into the Trump Account program while filing their 2025 taxes.

Parents can elect to create a Trump Account for their child during the tax filing process by using form 4547.

If you don’t want to file the form with your taxes, you can submit form 4547 at anytime via online portal that is scheduled to be available in the summer of 2026.

The IRS has stated that contributions—including the federal $1,000 and private $250—cannot be deposited until after July 4, 2026.

Accuracy Matters: Please be advised that “Trump Accounts” and the associated $250 gift are subject to finalized federal legislation and IRS implementation. At this time, there is no line on the 2024 or 2025 Form 1040 labeled “Trump Account.” We recommend maintaining records of your child’s SSN and birth certificate now, so you are ready to move quickly once the program is officially active.

Questions about your family’s eligibility? Contact Howard Tax Prep LLC today—We fix tax problems (and help you plan for the future).

Here in our Chicago South Loop Tax Preparation office and our Homewood Il Tax Preparation office, we work with homeowners and real estate investors that are looking to save on their taxes. As we always say, when it comes to taxes, the best tax benefit is a tax credit, because you receive the amount on a dollar-for-dollar basis, versus tax deductions which only slightly reduce your taxable income. To say it another way, a $2,000 tax credit saves you $2,000 in taxes.

Energy Efficient Home Improvement Credit

Per the IRS, “if you make qualified energy-efficient improvements to your home after Jan. 1, 2023, you may qualify for a tax credit up to $3,200.” The Efficient Home Improvement Credits help homeowners pay for various types of energy efficiency improvements. The credit is 30% of energy property cost up to $1,200, and $2,000 per year for qualified heat pumps, biomass stoves, or biomass boilers. Since more people will qualify for the energy-efficient improvements, we’ve outlined the details below.

Exterior doors (energy star approved). Max 2 doors, $250 each, total credit amount $500. Example, door cost $1,300; 30% of $1,300 is $390. Although 30% of the cost is $390, the taxpayer can only get $250 of the $390 (per door up to $500).

Exterior windows & skylights that meet Energy Star Most Efficient certification requirements; max credit amount $600.

Electric panel upgrades. 30% of the cost up to $600.

Home insulation. 30% of the cost up to $1,200.

Central air conditioner. 30% of the cost up to $600.

Furnace, heat pumps, water heaters, and hot water boilers. 30% of the cost.

Home energy audits. 30% of the cost up to $150.

Heat pumps, biomass stoves, or biomass boilers. $2,000 per year.

What if I earn a high income?

The great thing about this credit is that even those that earn higher incomes can take advantage of the credit (because there are no maximum income thresholds).

How many times can I claim this credit?

Although the Energy Efficient Home Improvement Credit has a $1,200 annual cap (with limits on specific items), you can claim the credit each year through 2033. Some homeowners are choosing to perform energy efficiency projects over several years, so that they can claim the credit each year.

Will this credit increase my tax refund?

It depends! The credit is nonrefundable, meaning if you don’t owe any tax, you will not receive the credit as a refund check. However, the credit can reduce what you owe, helping you to receive a refund of the income taxes withheld by your employer.

Can I carry this tax over to another year?

No, you can’t carry the credit over to a future tax year.

Who can claim the credit

Homeowners that use the property as their main residence, or a vacation home.

In our South Loop of Chicago Tax Preparation office, and our Homewood, Il tax preparation office, we often come across taxpayers that want to reduce their tax bill and save money (legally). Because we specialize in small business owner and real estate investor tax preparation & tax planning, we often come into contact with new landlords.

Most of your purchase costs when acquiring a rental property will be detailed in the real estate closing statement or the closing disclosure. The closing statement is a financial instrument, not a tax document.

You need to go through each line item in the statement and assign it to one of the three following tax categories:

Basis

Loan Acquisition

Operations

Then, once you have divided your expenditures into these three categories, you often need to consider the best tax strategies for each. For example, in the basis category, you assign costs to land, land improvements, buildings, and personal property. Each dollar assignment has an impact on your profits.

This article provides a useful guide of information to help you build your rental property profits on the day you close escrow.

1. Basis

Generally, your basis (a fancy way of saying the money you put into something) is the total cost you pay for the property, including your costs of obtaining and perfecting the title. Once you have this total cost, you allocate that cost to land, land improvements, buildings, and equipment, and then you depreciate all but the land.

1.1 What Goes into Basis

Examine the closing statement to identify expenditures that you should include in your basis. The following list gives you some of the items you usually would include:

Contract price

Personal property

Abstract (title search) fees

Escrow fees

Legal fees (for the title search, sales contract, and deed but not for the loan)

Real estate commissions (generally paid by the seller; include in your basis if paid by you, the

buyer)

Recording fees

Surveys

Transfer or stamp taxes

Title Examination

Amounts you paid on behalf of the seller, such as back taxes, back interest, recording fees,

mortgage fees, charges for improvements and repairs, and sales commissions

In addition to what appears on the closing statement, make a review of your credit card statements and checkbook

to identify other costs that apply to the purchase of this property.

1.2 Allocating Basis to Assets

You allocate basis to land, land improvements, buildings, and equipment based on fair market values at the time of purchase.

2. Loan Acquisition

When you buy rental property, tax law divides your loan costs into two categories:

Costs you incur to obtain the loan

Costs, like points, that decrease the mortgage interest rate

2.1 Costs to Obtain the Loan

You write off the costs of obtaining the mortgage over the life of the mortgage using the straight-line amortization method. Costs you include in this write-off include:

Mortgage commissions

Abstract fees

Mortgage recording fees

Mortgage stamp and other taxes

Credit report

Lender’s inspection report

Appraisal fee for the loan

Mortgage insurance application fee

Mortgage assumption fee

Example. You incur $8,000 in costs to obtain a 10-year mortgage loan. You deduct $800 a year.

Loan origination fees, brokers’ fees, maximum loan charges, and premium charges are not points. These are costs of obtaining the loan and, like the costs above, you amortize them on a straight-line basis over the life of the loan.

2.2 Loan Costs That You Treat Like Interest

Points. The term “points” is often confusing. In a financial sense, the point represents a prepayment that you make to obtain a discount on the loan interest rate. In general, the more points you pay, the lower the interest rate.

Essentially, the payment of points is the payment of interest in advance, and the tax law gives special treatment to your payment of points.

Since points are nothing more than prepayment of interest on your loan, tax law treats points as original issue discount (OID). The amount of your OID determines which method you may use to write off points paid on a rental property acquisition.

3. Operating Items

At closing, you might pay real property taxes, fire and property insurance premiums, and city and town taxes. Look at these expenses. See whether they apply to your current and future holding of the property. If so, you may deduct these costs as current-year operating expenses, assuming you place the property in service at closing.

Per IRS publication 551, “If you pay real estate taxes the seller owed on real property you bought, and the seller didn’t reimburse you, treat those taxes as part of your basis. You can’t deduct them as taxes. If you reimburse the seller for taxes the seller paid for you, you can usually deduct that amount as an expense in the year of purchase.”

You also want to look through your checkbook and credit card statements for other operating expenses and perhaps some start-up expenses.

Takeaways

The closing statement examination in this article is the perfect place to start your property on the track for maximum profits by getting the best tax benefits at inception.

When you are thinking about acquiring a rental property, make it a point to review this article so that you can get the most out of both your closing costs and your cost to buy the property.

Here in our South Loop Chicago Tax Preparation office, we assist new entrepreneurs with creating their business entity. Recently we have received questions regarding the new beneficial owner report that FINCEN will be requiring. This article will address the FINCEN business owner reports, the information required, and the businesses that must comply.

Effective January 1, 2024, the Corporate Transparency Act (CTA) will go into effect. If you already have an active small business or a rental property in an LLC that you started before 2024, you must comply with the new federal report filing requirements by December 31st, 2024.

If, in 2024, you start a new business or add a rental to a new LLC, you will have 90 days to comply with the new Federal reports filing requirement. Under this requirement, you have to file two reports simultaneously with the Federal Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN):

A “beneficial owner” information report (BOI report).

A company applicant information report.

Please note that this new federal filing is separate from state and local filings, such as your annual report. From now on, determining whether this filing is required, and completing it within the deadline must become a routine part of forming most new corporations and LLCs.

This brand-new federal beneficial owner information report (BOI report) will be filed with the Financial Crimes Enforcement Network (FinCEN)—the Treasury Department’s financial intelligence unit. The filing requirement applies to most corporations, limited liability companies, limited partnerships and certain other business entities.

These BOI reports must disclose the identities and provide contact information for all of the entity’s “beneficial owners”: the humans who either (1) control 25 percent of the ownership interests in the entity or (2) exercise substantial control over the entity.

Your BOI report must contain all the following information for each beneficial owner”:[1]

Full legal name

Date of birth

Complete current residential street address

A unique identifying number from either a current U.S. passport, state or local ID document, or driver’s license or, if the individual has none of those, a foreign passport

An image of the document from which the unique identifying number was obtained

What happens if I don’t comply?

First, there are civil penalties of up to $500 for each day that a violation continues (capped at $10,000). Second, there are also potential criminal penalties—imprisonment for up to two years for any person who willfully:

1.) provides, or attempts to provide, false or fraudulent beneficial ownership information and/or 2.) fails to report complete or updated beneficial ownership information to FinCEN.

The good news is that if make a mistake, you can avoid civil or criminal liability by submitting a corrected report within 90 days.

Who will have access to these reports?

FinCEN will create a new database called BOSS (Beneficial Ownership Secure System) for the BOI and will deploy the BOI to help law enforcement agencies prevent the use of anonymous shell companies for money laundering, tax evasion, terrorism, and other illegal purposes. It will not make the BOI reports publicly available.

Is my company a reporting company?

The CTA applies only to “reporting companies.” If the entity you’re forming is not a reporting company, you don’t have to worry about the CTA. Unfortunately, almost all small businesses are reporting companies.

Subject to some significant exemptions, the CTA applies to business entities formed by filing a document such as articles of incorporation or organization with a secretary of state office or similar official. This includes LLC’s corporations, limited partnerships in most states, and limited liability partnerships.

Breakdown of Business Entities & Their Reporting Requirements.

Sole proprietors. The CTA does not apply to sole proprietors because no document need be filed to legally establish a sole proprietorship (you simply start a business you own yourself).

Single-member LLCs. The CTA applies to individual business owners who form one-member LLCs to operate a business, even though that single-member LLC is taxed as a sole proprietorship (a “disregarded entity”). Reason: you must file a document (usually called articles of organization) with the secretary of state to form a one-member LLC, just as you must for multi-member LLCs.

Rental property. Many individuals form LLCs to own their rental properties. The newly formed 2024 LLCs trigger the CTA reporting requirements.

General partnerships. The CTA does not apply to general partnerships, except in a few states such as Delaware where general partnerships must make a state filing to come into existence. In states where the general partnership filing is optional and the partnership makes the filing, it must file the BOI.

Business trusts. Most business trusts are not reporting companies since no government filings are required to create them. But there are exceptions, such as Delaware statutory trusts.

Foreign corporations. The CTA also applies to foreign corporations, LLCs, and other entities that register to do business in the U.S. This is ordinarily done by filing a document with the state’s secretary of state.

Small businesses. Not all LLCs, corporations, or other business entities are subject to the CTA. Its focus is on smaller businesses not already heavily regulated by the federal government. FinCEN estimates that of the approximately 5,616,000 new companies formed each year, about 617,894 will be exempt. The broadest exemption is for “large operating companies.” These are businesses with:

more than 20 full-time employees (those who work more than 30 hours per week),

$5 million in domestic gross receipts or sales on their prior-year tax return, and a physical presence in the U.S

tax-exempt non-profits, including Section 501(c)(3) corporations, and Section 527 political organizations.

What happens if I change my business address or personal address?

You will have to file an updated BOI Report. The BOI updated filing will need to be renewed if any of the information on the BOI report changes. If there is a change in the information on the BOI report, an updated report must be filed within 30 days of the change.

Summer is fast approaching, and with the weather change, businesses will soon be hosting office picnics, award ceremonies, and holiday parties. As is the only constant in tax matters, there are changes (again) in what meals the IRS will allow small business owners to deduct at 100% or 50%. Here in our Chicago South Loop Tax Preparation and our Homewood Il, Tax preparation offices, since you no longer can deduct all restaurant meals at 100%, we’ve done the research for you so that you can plan accordingly when organizing an office outing, having a business lunch, or providing meals for an employee meeting.

As you may already know, there have been some major changes to the business meal deduction for 2023 and beyond. The deduction for business meals has been reduced to 50 percent, a significant change from the previous 100 percent deduction for business meals in and from restaurants, which was applicable only for the years 2021 and 2022 due to Covid.

To help you better understand what you can deduct, please see the table below:

Amount Deductible for Tax Year 2023 and Beyond

Description

100%

50%

Zero

Restaurant meals with clients and prospects

X

Entertainment such as baseball and football games with clients and prospects

X

Employee meals for the convenience of the employer, served by an in-house cafeteria

X

Employee meals for required business meetings, purchased from a restaurant

X

Meal served at the chamber of commerce meeting held in a hotel meeting room

X

Meal consumed in a fancy restaurant while in overnight business travel status

X

Meals cooked by you in your hotel room kitchen while traveling away from home overnight

X

Year-end party for employees and spouses

X

Golf outing for employees and spouses

X

Year-end party for customers

X

Meals made on premises for the general public at a marketing presentation

X

Team-building recreational event for all employees

X

Golf or theater outing or football game with your best customer

X

Meal with a prospective customer at a country club following your non-deductible round of golf

X

Chart of what meals you can deduct at 100% and what you can deduct at 50%.